Salary or dividends in an LTD in 2026/27. How much do you really take home?

Daria runs a creative business. She organizes Crochet & Knitting classes, runs a weekly Crochet Club, sells crochet patterns, and creates YouTube tutorials. The business is growing, clients are coming in, money is flowing into the account, and a question familiar to many UK business owners is increasingly arising:

is it better to operate as a self-employed individual or through an LTD company?

An even more important question is: how much money Daria keeps personally after all taxes?

Because clients usually aren't just interested in whether a tax is called Corporation Tax, Income Tax, National Insurance, or Dividend Tax. What clients want is a simple answer:

"If the business earns £60,000, how much do I ultimately get to keep?"

In this article, we compare three main scenarios.

The first scenario is Daria as a self-employed individual.

The second scenario is Daria running an LTD company, paying herself a low salary of £12,570 and the rest as dividends.

The third scenario is Daria running an LTD company and paying out everything via PAYE as a salary.

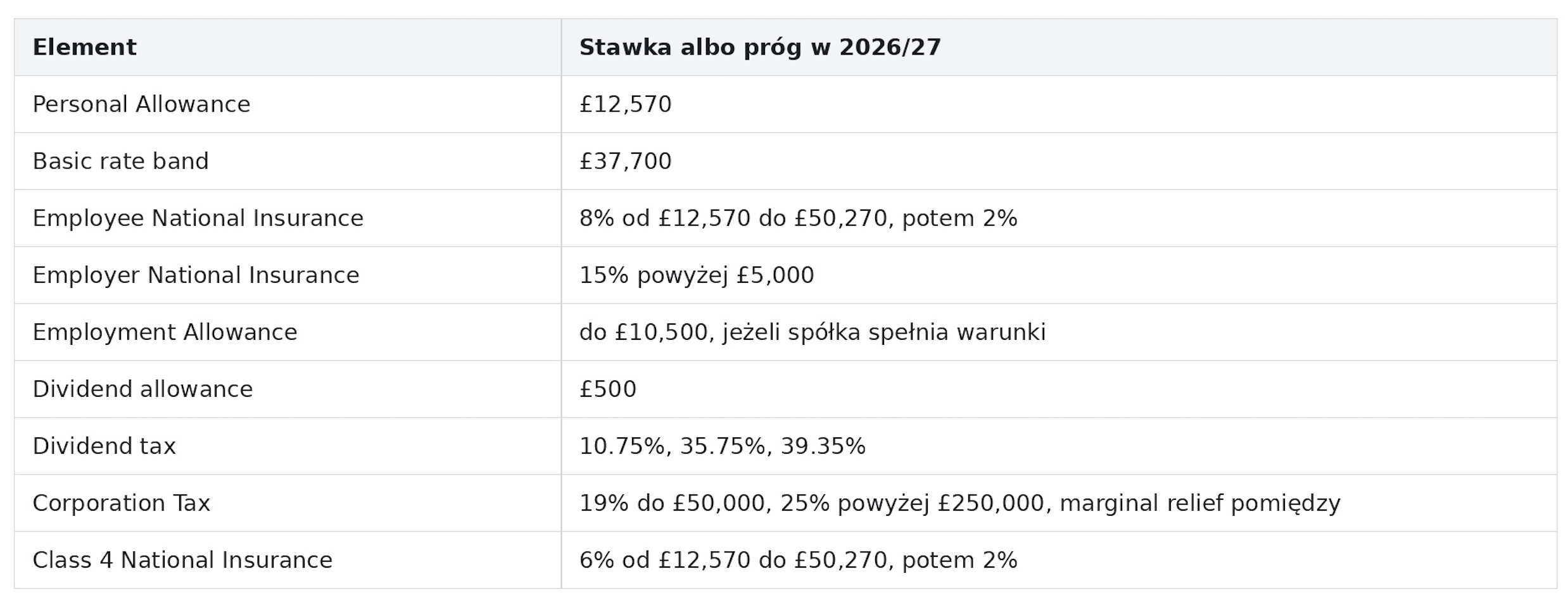

For simplicity, we assume Daria is a UK tax resident, lives in England, Wales, or Northern Ireland, has no other income, no student loan, and we are not analyzing VAT, pension contributions, or other reliefs. We assume the business has £60,000 profit before Daria's payout. For an LTD company, this means £60,000 profit before the director's salary. Dividend rates from 6 April 2026 are 10.75% for the basic rate, 35.75% for the higher rate, and 39.35% for the additional rate, with a dividend allowance of £500.

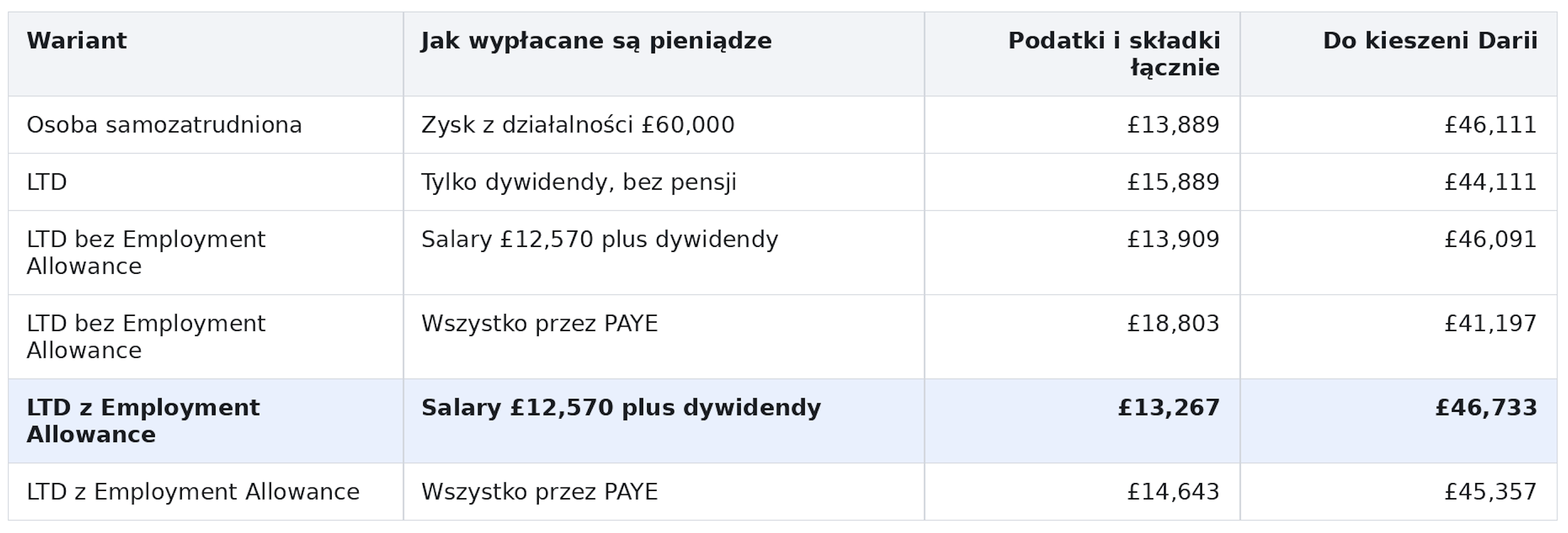

First, the most important table: how much does Daria get to keep?

The conclusion is interesting. With £60,000 profit and no Employment Allowance, the difference between self-employment and an LTD company with a low salary and dividends is very small.

In our example, a self-employed individual receives approximately £46,111, while an LTD company with a salary of £12,570 and dividends yields approximately £46,091. This shows that after the dividend tax increase in 2026/27, an LTD company doesn't always offer a huge tax advantage if the owner extracts all profit personally.

But this doesn't mean an LTD company makes no sense. It means you need to calculate your specific situation. An LTD company can make sense for other reasons, for example, when some money remains within the company, when the business wants to appear more professional, when a different legal structure is needed, or when Daria plans for growth.

What rates do we use in the calculation?

PAYE and employee National Insurance thresholds, as well as employer National Insurance for 2026/27, are confirmed in employer guidance, and the Employment Allowance is £10,500. Corporation Tax is 19% for small profits up to £50,000, 25% for profits above £250,000, with marginal relief applying between these levels. For the self-employed, Class 4 National Insurance in 2026/27 is 6% between £12,570 and £50,270, and 2% above £50,270.

Scenario one: Daria as a self-employed individual

If Daria operates as a self-employed individual, she does not pay herself a salary or dividends. Her business profit is her income. From this, she pays Income Tax and Class 4 National Insurance.

Let's assume that her profit from workshops, crochet patterns, the Crochet Club, and tutorials is £60,000.

The most important thing in this scenario is that Daria pays tax on the entire profit. There is no Corporation Tax, no dividends, and no payroll for her as a director. It's simply business profit, Income Tax, and Class 4 National Insurance.

Scenario two: Daria has a LTD and pays herself a £12,570 salary plus dividends

Now, let's assume Daria runs the same business through a LTD. The company has £60,000 profit before her salary. Daria is the sole director and the only person on the payroll, so we assume the company does not have Employment Allowance. This is important because single-director companies where the director is the only person on the payroll generally cannot claim Employment Allowance.

Daria pays herself a salary of £12,570. From this salary, she personally pays no Income Tax or employee National Insurance, as it falls within her Personal Allowance and Primary Threshold. However, the company pays employer National Insurance because the Secondary Threshold is £5,000.

This scenario is very close to self-employment. The difference in our example is about £20 in favour of self-employment. For many clients, this will be a surprise, as for years they've heard that a LTD always yields a much better tax outcome. In 2026/27, with increased dividend tax and a low employer National Insurance threshold, it simply needs to be calculated.

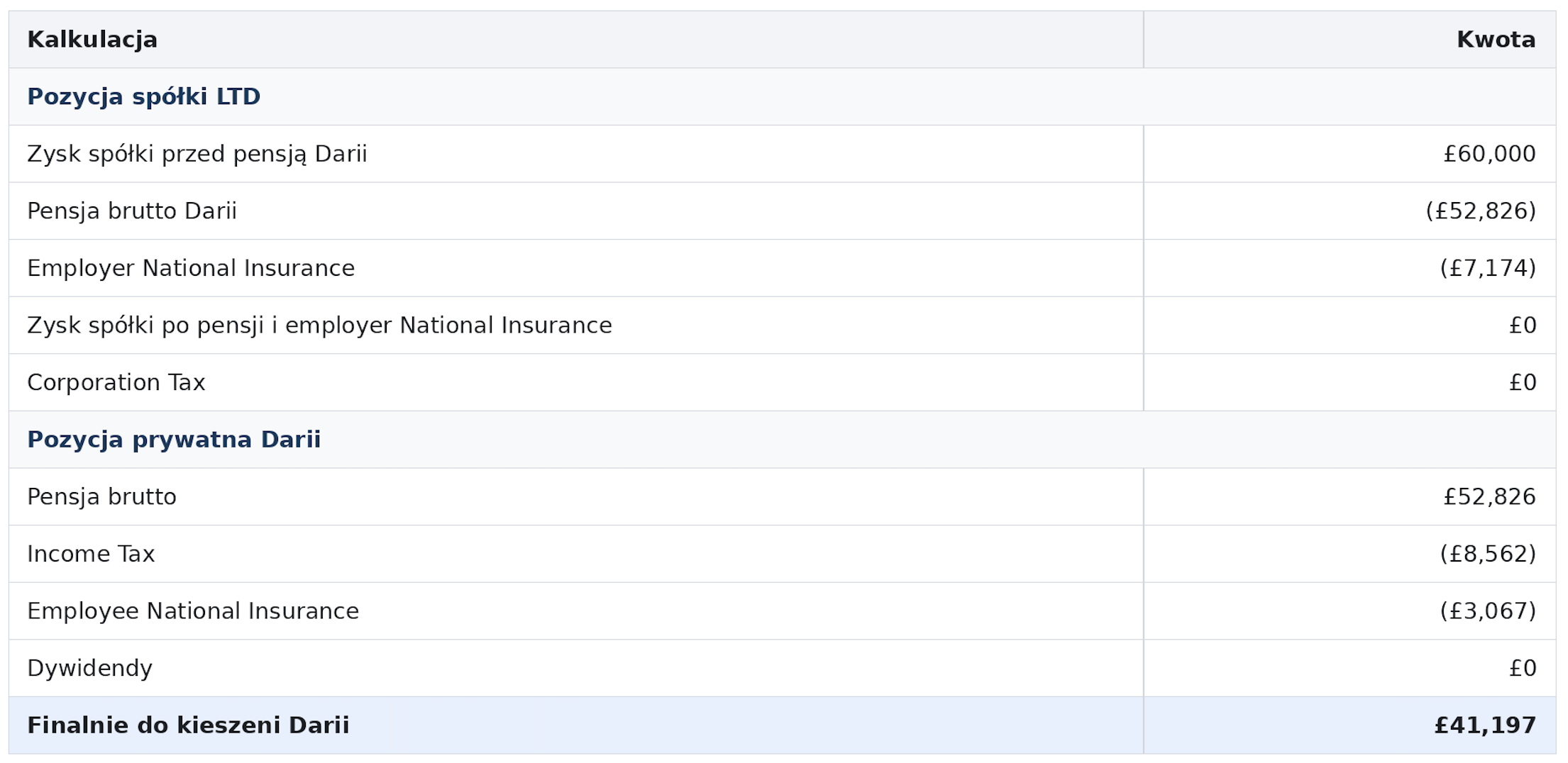

Scenario three: Daria has a LTD and pays out everything via PAYE

Now let's see what happens if Daria doesn't pay dividends but wants to take everything out as a salary via PAYE. This sounds simple, but it's usually less tax-efficient because Income Tax, employee National Insurance, and employer National Insurance all come into play.

The company has £60,000 available for the cost of salary and employer National Insurance. This means Daria cannot receive exactly £60,000 gross salary, as the company would still have to pay employer National Insurance. Under our assumptions, the gross salary is approximately £52,826, and employer National Insurance is approximately £7,174.

This scenario performs the worst. Daria receives approximately £41,197, which is about £4,894 less than in the scenario with a low salary and dividends, and about £4,914 less than as a self-employed individual.

What if Daria's company has Employment Allowance?

This is very important because Employment Allowance can change the outcome. If Daria has a genuine employee, for example, someone assisting with workshops, administration, or teaching, and the company meets the Employment Allowance conditions, then the company can reduce its employer National Insurance by up to £10,500 annually. However, this cannot be assumed automatically, as a single-director LTD with only the director on the payroll usually does not qualify for this allowance.

If Employment Allowance is available, the scenario with a £12,570 salary and dividends looks like this.

In this scenario, the LTD with a low salary and dividends outperforms self-employment by approximately £622. This is still not a huge difference for £60,000 profit, but the outcome is clearly better.

For comparison, if Daria paid out everything via PAYE with Employment Allowance, she would receive approximately £45,357.

Even with Employment Allowance, PAYE alone still results in less take-home pay than a low salary plus dividends.

Why a low salary plus dividends can still work?

A salary of £12,570 works because it utilizes the Personal Allowance and Primary Threshold. Daria doesn't pay Income Tax or employee National Insurance on this salary. At the same time, the salary is a company expense, so it reduces Corporation Tax.

Dividends work differently. A dividend is not a company expense. First, the company pays Corporation Tax, and only then can it pay out a dividend from the post-tax profit. Daria pays personal dividend tax on it.

That's why you can't look at just one rate. If someone tells Daria, "Dividends only have a 10.75% tax," that's not the full picture. Before the dividend, the company also paid Corporation Tax. If someone says, "Salary is bad because of employer National Insurance," that's also not the full picture. Salary reduces Corporation Tax.

The simplest comparison looks like this.

The most important takeaway for an LTD owner

If you run a single-person LTD, don't employ anyone, are the sole director, and the only person in the company, then you are not entitled to Employment Allowance.

This means that when you pay yourself a salary via PAYE, the company may pay employer National Insurance already above the Secondary Threshold. In 2026/27, this threshold is £5,000, and employer National Insurance is 15%. Employment Allowance can reduce employer National Insurance by up to £10,500 annually, but a single-person company with only the director on payroll usually won't benefit from this.

And that's why, in our example, a single-person LTD almost doesn't add up tax-wise if we only look at the money Daria gets in her pocket. As a self-employed person, Daria receives approximately £46,111 net. As the owner of a single-person LTD without Employment Allowance, with a salary of £12,570 and dividends, she receives approximately £46,091 net. The difference is about £20. For the client, this is practically the same amount of money.

But here's a very important element that isn't visible in the tax calculation itself.

Running an LTD is usually more expensive accounting-wise than operating as self-employed. The company has more obligations, more documents, accounts, Corporation Tax return, payroll, dividends, director loan account, confirmation statement, and formalities.

Therefore, if a single-person LTD gives Daria practically the same net result as self-employed, and at the same time costs more in accounting services, then at such a profit level and when paying out all the money privately, an LTD may not provide a real tax benefit.

That's why one shouldn't automatically tell a client today: „set up an LTD, because it will be better tax-wise”.

In 2026/27, this might be true, but only in some situations. If the company has Employment Allowance, employs actual staff, leaves part of the profit in the company, invests, builds a larger business, or has other business reasons, an LTD might make sense. But if we're talking about one person who works alone, doesn't employ anyone, and wants to pay out all the profit to themselves every year, then our calculations show a simple thing: in terms of money in your pocket, self-employed can give practically the same result as a single-person LTD, and sometimes even better after accounting for bookkeeping costs.

The simplest way to put it is:

if you are alone in an LTD, don't have Employment Allowance, and pay out all the profit privately, the LTD company itself is no longer an automatic way to achieve significant tax savings.

In our example, Daria, as self-employed, takes home approximately £46,111, while Daria, operating as a sole director LTD without Employment Allowance, takes home around £46,091. If we add the higher accounting costs for an LTD, then for many small sole-person businesses, the answer might be very simple: from a tax perspective, being self-employed might be more sensible than an LTD.

This is precisely why the decision to form an LTD shouldn't be based on the old adage 'a limited company always pays off'. Today, you need to calculate the specific situation: how much the company earns, whether it employs people, whether it has Employment Allowance, whether the owner withdraws all profits, how much accounting costs, and how much money the owner ultimately keeps personally.