Company profits or self-employment income?

Let's clarify a fundamental point regarding the Corporation Tax increase. The 25% tax will only apply to companies whose annual profit exceeds £250,000.

Dividend Tax vs. Salaries in the UK

Will the Corporation Tax (CT) changes, effective from April 2023, reduce the tax efficiency of dividends compared to salaries? Higher rates of this tax might mean it's time to consider whether operating as a limited company is still tax-advantageous. Many tax experts are already predicting a shift away from small director-managed companies towards self-employment (independent contractors and partnerships).

Will all businesses become tax inefficient?

Many factors can influence a change in tax position, both positively and negatively. For example, the size of anticipated business profits/income, what other taxable income is earned, and what expenses affecting the tax base are incurred.

Tip. One way to maximize tax efficiency is to split your business income between your company and self-employment, in the most advantageous way for both.

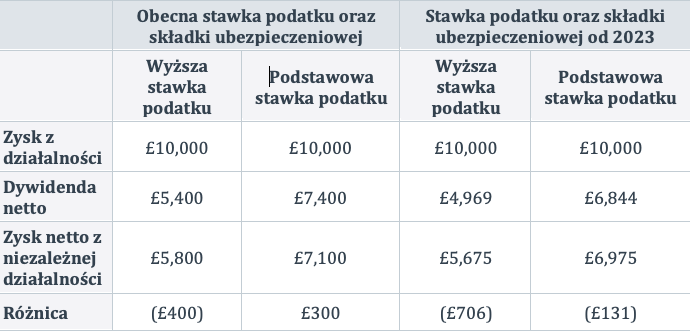

The table compares tax and National Insurance liabilities for dividend income and self-employment profits. To do this, we calculated the net income a business owner would receive from a £10,000 dividend and from the same amount of self-employment profit. We compare the situation with current tax and National Insurance rates against the situation from April 2023, when higher rates will apply.

Tax Rate vs. Dividends in the UK

The table shows that, under current rules, a freelancer with profits subject to the basic tax rate will be in a less advantageous position compared to a company with profits paid out as dividends, with a difference of £300 for every £10,000 subject to tax. For profits exceeding the higher tax threshold, the situation reverses, with a difference of £400 per £10,000. From April 2023, regardless of the tax rate applicable to the entrepreneur, the difference will be £706 and £131 per £10,000, respectively. As mentioned earlier, other factors influence the comparison of tax and National Insurance liabilities for dividends versus self-employment profits, which could improve the net outcome. Nevertheless, the trend is as shown in the above summary.

Tip. The ideal solution is to keep company profits intended for dividend distribution close to the basic rate limit and generate further income through self-employment. This can be achieved by:

- self-employment independent of your company

- freelancing work for your own company.

Any plans to change your business structure should always be discussed with an accountant or tax advisor before taking further action.